FAQs

-

Upon The Death of a Loved One

-

If someone dies without a will, does all their property go to the State?

No. There are specific laws regarding which family members are entitled to receive a decedent’s property if that person dies without a will. Click here to see a chart that explains who is entitled to the estate.

-

My loved one did not have a will. What happens next?

New York State has specific laws that cover the distribution of a decedent’s assets if he or she dies without a will. The law also determines the selection of the person who will act as “Administrator” of the estate and have the authority to handle estate matters. However, this does not happen automatically, and someone must petition the Surrogate’s Court in the county where the decedent was domiciled to be appointed as “Administrator.” A consultation with an attorney who practices in the area of probate or trusts and estates can be very helpful in this situation.

-

My loved one had a will. What should I do now?

The person who is nominated as Executor in the will usually petitions the court for probate. This does not happen automatically, and may not be necessary in every case. A consultation with an attorney who practices in the area of probate or trusts and estates can be very helpful at this point. If you are in possession of the original will, whatever you do, DO NOT UNSTAPLE OR REMOVE THE BINDINGS OF THE WILL.

-

My parent just passed away. What should we do?

Your first priority in the time of grieving should be focused on the funeral arrangements. You should determine whether or not your loved one had pre-planned funeral arrangements and/or a cemetery plot deed. When the immediate arrangements have been taken care of, you should schedule a consultation with an attorney who can assist you with the probate or estate administration process.

-

What are the advantages of a leaving your children’s inheritance in trust instead of distributing it outright?A Descendants Trust, also sometimes referred to as an Inheritance Protection Trust is a type of irrevocable trust that manages your children’s inheritance in trust rather than giving them outright distributions. This type of trust has many advantages, such as:

- If properly structured, the trust assets can be exempt from federal estate tax when the beneficiary passes.

- The trust assets are considered separate marital property and therefore are protected in the case of divorce.

- The trust assets are protected from creditors of the beneficiary.

- It is more likely that the assets stay within the family bloodline.

- You can direct management of the trust to be as restrictive or as flexible as you would like.

-

The bank says I need Letters Testamentary to access my deceased parent’s account. Can’t I use a Power of Attorney?

No. A Durable Power of Attorney terminates when the principal dies. There is an abridged process to obtain smaller amounts of money from a deceased parent’s bank account, but for larger estates, the bank needs legal confirmation of who is authorized to receive the funds. Letters Testamentary are issued by the Surrogate’s Court to the nominated Executor of a will when the will has been accepted by the court for probate. The “Letters Testamentary” (or Letters of Administration if there is no will) indicate the Executor’s (or Administrator’s, if there is no will) authority to act in connection with the decedent’s estate. The only way to obtain Letters Testamentary is through a probate (or administration) proceeding in the Surrogate’s court.

-

The police sealed the apartment/house. How can I enter?

It would be important to enter the premises to find funeral and burial information, insurance policies, and a will. You will have to file a petition to enter the property at the Miscellaneous Department of the Surrogate’s Court in the county where the decedent lived. When the court order is issued, you should contact the police precinct that holds the keys and follow their instructions.

-

What is the estate tax exemption?Currently, in 2023, if a NY estate is less than $6,580,000, there is no estate tax. New York does not have gift tax, but will “claw back”, or include, any gifts made within three years of date of death when calculating the value of the estate for estate tax purposes. If an estate is more than 3% over that exemption amount (more than $6.9MM), the exemption is lost and the entire estate is taxed from dollar 1 (sliding scale up to 16%). There are strategies to reduce or even eliminate this tax with proper advance planning.

Currently, the Federal gift and estate tax exemption amount is $12.92 million per person. Tax is calculated on the amount the decedent had a death PLUS gifts made by the decedent during lifetime that were above the annual exclusion amount. In 2023, the annual gift tax exclusion amount is $17,000. That means that the first $17,000 gifted to an individual is not counted towards lifetime gift amount, but anything above that gifted to the individual would be added to the lifetime amount). The Federal Tax rate is 40%, which is assessed on the portion of the estate that is above the estate and gift exemption amount. The Federal exemption amount is slated to be reduced significantly in 2026.

-

How much tax would I pay on an inheritance?

If you are a resident of New York, then, none. New York State does not have inheritance tax. Further, there is no federal inheritance tax. That means that a person that is a resident in New York can inherit any sum of money without being subject to any inheritance tax. There are federal and state estate taxes, though, if an estate is above the estate tax exemption amounts. Taxes are assessed on the value of the deceased person’s estate and would be paid from the estate, before being distributed to the beneficiaries of the estate (or trust). That being said, it could be the responsibility of beneficiaries to pay the estate’s tax from assets that they have inherited, if there are no estate funds to cover the assessed taxes due.

-

What estate planning options do I have for my pet/s?

Since the law considers animals to be property, you cannot leave money to your pets but you can still ensure they have a good life after your death. You can use your estate planning devices to give your pets to a specified person or organization. Additionally, you can set aside money from your estate, for example by utilizing a Pet Trust, to make sure the new caretaker has the resources to take good care of your pet.

-

-

When A Loved One Needs Long Term Care

-

What is the Medicaid five-year look back period?

When you apply for Medicaid in the state of New York, the New York State Department of Health reviews all gifts given and transfer of assets from the past five years to determine how long the applicant must wait before receiving Medicaid benefits. Since the five-year look back period can affect a loved one’s long term care options, is advisable to consult with an elder law attorney before the long-term care is actually needed.

-

The nursing home says that they will prepare the Medicaid application for free. Why should I be hesitant to use their services?

In New York it is true that you don’t have to use an attorney to prepare a Medicaid application. In fact, you can do it yourself. But remember that the law has many nuances and intricacies. Imagine having a nursing home prepare and submit your parent’s Medicaid application, and it is approved. But after parent’s death, you find out that a lien has been placed on your parent’s house in the amount of the benefits which Medicaid paid out for your parent. Nobody advised you that the house could have been protected under the law under one of the Medicaid exceptions to the transfer of assets rules. While someone who works for a nursing home may have the best interests of the nursing home in mind while preparing your Medicaid application, an attorney that you hire to represent you has an ethical duty to advocate for you and your interests. Furthermore, while it is legal for the nursing home, or a non-attorney Medicaid expediter assist you with your Medicaid application, they are not authorized by law to give you legal advice to maximize the protection of your assets in the process of accessing Medicaid benefits. Having an attorney advise you how to best protect your assets, using different techniques and exceptions to the transfer of assets rules, may ultimately result in savings exponentially greater than the attorney’s fee. And vice versa, failure to use the assistance of an attorney can potentially have results to the opposite effect.

-

Is Medicaid planning legal?

Absolutely yes. Elder law attorneys work within the guidelines of the law to help you qualify for benefits. There are many legal planning opportunities that an elder law attorney can implement for you or your loved one should the need for long term care arise.

-

My parent is able to live at home, but needs health aides. They have plenty of savings—should we consider Medicaid?

Yes. Eligibility rules are different for Medicaid home care than for Medicaid nursing home care, and it is possible your parent may very well qualify for Medicaid home care fairly easily.

-

My parent has plenty of savings. Won’t they be able to pay the nursing home without Medicaid?

Maybe, but the New York State Department of Health lists the annual estimated average nursing home rate in 2023 at $169,632 on Long Island and $169,704 for New York City. Most people without unlimited wealth who enter a nursing home will eventually have to rely on Medicaid to assist in payment of their health care. If you or a loved one are searching for the right nursing home, please be sure to take a look at this checklist for help.

-

My parent has been admitted to a nursing home. The social worker is talking about Medicaid. Can my parent qualify for Medicaid?

Yes, most likely he or she can. Medicaid is a “means tested government entitlement.” In plain language, this means that a person’s income and resources must be below a certain level in order to be eligible for benefits, among other eligibility requirements. With proper planning, a person can protect his or her assets. Many people are often misinformed regarding Medicaid planning issues, and think that there is nothing they can do to protect their assets and must first spend them down to pay for their nursing home fees until they are below the Medicaid level of assets limit. This is almost always not true! In most cases, at least some assets can be protected even at a very late date. However, the earlier the planning is started, generally the more assets can be protected.

-

What is the income and asset limit for Medicaid eligibility?

The answer varies by state. In New York, in order to be eligible for Medicaid, there is an asset limit of $30,182. There are ruled relating to income that are different for community care and nursing home care. Even if you have income or assets greater than the Medicaid eligibility limits, there are options to plan to allow you to protect your finances and become eligible for Medicaid long term care services.

-

What transfers during the Medicaid look back period are exempt from being penalized?Transfer penalties for transfers made for less than full consideration are not imposed on exempt transfers made during the Medicaid lookback period. Such exempt transfers include transfers to a spouse, disabled child, or to certain exempt trusts. In addition, a person’s primary residence can be transferred without penalty to:

- A spouse

- A child under the age of 21 years old

- A blind or disabled child of any age

- A sibling with equity interest in the home and lived in the home for at least one full year immediately preceding the Medicaid applicant’s institutional care

- An adult child that lived in the home for at least two full years immediately preceding the Medicaid applicant’s institutionalization to care for his parent which delayed the need for the institutional care

-

Is the Medicaid 5-year look back period going to apply to Community Medicaid also? If so, when?

Currently, Medicaid’s 5-year look back period applies only to Institutional Medicaid but that may be changing. New York proposed legislation to implement a 30 month (2.5 year) look back period for Medicaid applicants looking to be approved for Community Medicaid. It is important to note that this is just a proposed legislation that the earliest It is expected to go into effect is April of 2024, but unofficially, there is information that it would be delayed even further.

-

-

When A Loved One Has Special Needs

-

Why should my special needs loved one access Medicaid even if money is not a factor?

There are many public benefits available to individuals with disabilities. While a family could have substantial wealth and believe that their loved ones with special needs would never need to access government benefits, they could be making a serious miscalculation. While most of a disabled individual’s needs could be met with private insurance and private pay, there are several excellent benefits that can only be accessed through Medicaid programs and cannot be paid for privately. Some of these programs may include community habilitation programs (providing skills and support in the home or community), day habilitation programs, eligibility for group home residency, and supported employment and employment training programs. Medicaid has strict financial requirements for eligibility. Therefore, even if some planning would be required, it may be a very worthwhile endeavor to pursue Medicaid eligibility to provide benefits and opportunities for your loved one that money itself can’t buy.

-

I keep hearing that it is very important to begin supplemental needs planning as soon as possible. Why is this?

By taking appropriate estate planning steps, you may ensure the future and the ability of a person with mental illness or other disabilities, who needs or is receiving public benefits, to live comfortably when you’re no longer around to be the caregiver. At the same time, you may preserve governmental benefits that will pay for essential things like medical treatments, prescriptions, special residential arrangements, and the like, while the funds you leave may be used for supplemental items or “extras” not covered by governmental benefits.

-

What is a Supplemental Needs Trust (SNT)?

This is a trust, which is created by an attorney that can be funded by a family member, an inheritance, insurance policy or other assets. It is used to supplement public benefits by paying for extra items that are not covered by Medicaid or SSI, such as vacations, computers and other items to enhance a beneficiary’s quality of life.

-

How are the funds in the Supplemental Needs Trust used for the person with a disability?

The Trustee would pay for items to benefit the beneficiary that are generally not provided by public benefits. By way of example, distributions might be made for expenses associated with household goods, recreational equipment, entertainment, and travel expenses.

-

What is the difference between a first party and third party SNT?

A first party Supplemental Needs Trust is created with the funds of a person with a disability under age 65, and would have a pay-back provision reimbursing the state at the beneficiary’s death for Medicaid assistance provided. A third party Supplemental Needs Trust created with funds of someone other than the beneficiary and does not have a pay-back provision. If advance planning was not done, and a person died leaving an inheritance for a disabled individual, a third party trust would no longer be an option, and the disabled individual may have no alternative other than funding a first party trust to preserve his government benefits.

-

Why do I have to plan in advance ifmy special needs child can create a first-party trust with their inheritance?

If your child receives an inheritance from your estate without advance special needs planning, his or her government benefits will immediately be at risk upon your passing. Imagine the trauma of losing a parent, often a primary care-taker and simultaneously having the stress of potentially losing government benefits and requiring the need for immediate, and likely costly, legal planning. Even with immediate legal planning at that time, often, the only option is creating a “first party” special needs trust, which assets would be subject to Medicaid payback upon the child’s death. On the other hand, you can plan in advance to protect your child’s inheritance immediately upon your death by establishing a supplemental needs trust under your will, or a standalone “third party” special needs trust that would be a seamless receptible for the inheritance.

-

What is the letter of intent that accompanies the Supplemental Needs Trust and why is it important?

This is a written statement drawn up by the person creating the trust (the “grantor”, often a parent of the beneficiary), that outlines the wishes of the parents as to how the money in the Supplemental Needs Trust should be used for the beneficiary, where the beneficiary should live, how the residence will be maintained, who will monitor the care and any other items important to the grantor. Weight will be given to the grantor’s intent in the creation of the trust if a situation arises and it is unclear on how to proceed in trust administration.

-

-

What Do I Need To Know About Trusts?

-

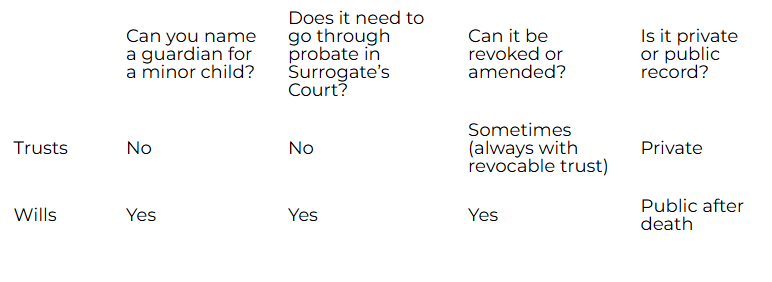

What is the difference between a will and a trust for asset distribution purposes?

Both a will and a trust are effective estate planning documents that guide the disposition of one’s assets, but in different ways. Both a trust and a will are legal documents that express an individual’s wishes as to the distribution of his or her assets after lifetime. But whereas a will would only go into effect after the individual’s lifetime, and only through a court process known as “probate,” a trust is a legal entity of its own that can be established and take effect during an individual’s lifetime, and avoid the court process for any assets transferred to the trust during lifetime. It is common to prepare both a will and a trust in estate planning. Here are some main differences between a trust and a will:

-

What is a trust?

A trust agreement is a document that gives clear instructions that you want followed for property held in the trust for your beneficiaries. Common objectives for trusts are to avoid probate, to reduce the estate tax liability, to protect your property for long term care planning, or to control specific distribution of your estate even after your lifetime. There are three important parties to a trust. The first is the “grantor” or “settlor”, which is the person(s) who is creating the trust. The grantor creates the trust and puts his or her chosen assets into the trust. The second is the “trustee”, the person(s) the grantor chooses to manage the assets in the trust. The grantor appoints the trustee to take good care of the assets in the trust according to the instructions written in the trust document. The third is the “beneficiary” or “beneficiaries”, the person(s) for whose benefit the assets are held and managed. The trustee has the duty and authority to manage the assets for the benefit of the beneficiary, who is entitled to receive the assets in the amounts, percentages, and at the time indicated in the trust. It is common for one person to play more than one role in a trust.

-

What’s the difference between an irrevocable trust and a revocable trust?

As you might guess, an irrevocable trust cannot be changed or revoked. Some of the reasons irrevocable trusts are used are for asset protection purposes such as estate tax planning or long term care planning. While you will not retain control of your assets with an irrevocable trust, there are still tools that can be implemented to allow you to retain a level of control such as changing your ultimate beneficiaries, or removing and replacing a trustee if you are not happy with their trust administration. However, it is the general relinquishment of control that enables you to qualify for Medicaid benefits or minimize estate taxes. As with any legal document, always be sure you completely understand how your irrevocable trust works before signing it and transferring your assets into it.

-

I hear that living trusts are much more expensive than wills.

While it is true that the legal fee to prepare a trust may be higher than preparation of a will, keep in mind that probate will most likely cost more in attorney’s fees, court fees, time and loss of control. In addition, you are likely preparing a trust for additional valuable benefits that far outweigh the cost of setting up the trust, such as protecting your assets, more specific control of your assets after your lifetime, minimizing the chance of a challenge to your will by a disgruntled family member, or minimizing taxes.

-

Isn’t it true that trusts are only for very wealthy people?

Not quite. A trust could be an appropriate part of the estate plan of anyone who owns property (including real estate, bank accounts, brokerage accounts and other investments, etc.). You don’t have to be wealthy to enjoy the advantages of a trust, such as avoiding probate, protecting your assets due to your incapacity, protecting your assets in the context of Medicaid planning, and keeping your estate plan private and out the public eye and the courts.

-

If I transfer my home into the trust, will I have difficulty selling it because the trust owns it?Not at all.

-

How do my assets get “into” my trust?

You will have to change titles on your real estate and other assets with formal titles such as bank accounts, stocks, other investments. This is not difficult, and our office can help you. Transferring real estate will require preparation and recording of a new deed and transfer tax documents. Each financial institution has its own process, but it can be as simple as giving instructions to the bank to change the name of the owner on your account. Sometimes your objectives can be accomplished without actually retitling assets, but simply designating the trust as beneficiary. An attorney can advise you on the best process in your particular situation. Remember, a trust will not achieve your objectives if you do not actually retitle your assets appropriately. An integral component of the estate planning process is funding your trust.

-

Will I lose control of my assets?

If you are the trustee of your revocable trust, then you still have full control and authority over the assets you choose to place in your trust. If you are preparing and funding a trust for long term care asset protection or for tax planning, then yes, you will be relinquishing a certain amount of control. Remember, if you still controlled the assets in the trust, then Medicaid (or the IRS) will still consider them yours and your objective wouldn’t be accomplished.

-

I have a will. Why would I need a trust if I my assets are below the Federal and New York State estate tax exemption amounts?

First of all, you may be right. A trust is not for everyone and your particular situation should be evaluated by a qualified attorney experienced with trusts. That being said, there are several reasons a trust may benefit you even if you have no estate tax exposure. After you die, the court must be petitioned to “probate” your will. Probate is the process by which your will is declared valid by the court, your executor is given authority, and the court makes sure that your wishes as stated in your will are carried out. Probate takes time, can be quite expensive, and is a matter of public record, so you lose control of privacy and your loved ones may need to wait a long time before they could administer your estate (i.e. sell your house, access your bank accounts, etc.). A “living trust” (a trust created during your lifetime) can avoid these issues and make it much easier for those who survive you. Also, a will has no effect until after you die. A living trust can keep control of your assets out of the courts if you become incapacitated. As an alternative to a power of attorney, or the need for someone to petition the court to appoint a guardian for you, the successor trustee (if you were the trustee of your own revocable trust) can seamlessly step in to manage the assets in your trust at your incapacity. In addition, there are a variety of other reasons a trust can be extremely beneficial to your estate plan, controlling the specific distribution or administration of your assets for a period of time after your death, for long term care asset protection (Medicaid planning), to hold in trust for a minor, to avoid the distributions in your estate from being challenged, to protect the inheritance of a beneficiary with special needs, or a beneficiary with a substance abuse problem, to name just a few reasons.

-

What are the benefits of leaving your children’s inheritance in a trust vs. giving it to them outright?A Descendants Trust, also sometimes referred to as an Inheritance Protection Trust is a type of irrevocable trust that manages your children’s inheritance in trust rather than giving them outright distributions. This type of trust has many advantages, such as:

- If properly structured, the trust assets can be exempt from federal estate tax when the beneficiary passes.

- The trust assets are considered separate marital property and therefore are protected in the case of divorce.

- The trust assets are protected from creditors of the beneficiary.

- It is more likely that the assets stay within the family bloodline.

- You can direct management of the trust to be as restrictive or as flexible as you would like.

-

-

What Do I Need To Know About Wills?

-

Can I just fill out a template for a will I found online?The laws in New York state have very specific rules regarding what makes a will valid, both in the way it is written and the way it is signed. A will which is not prepared under the supervision of an attorney runs the strong risk of being declared invalid after your passing, at which time it is too late to fix.

-

Instead of writing a will, why can’t I just make my heirs co-owners of my property while I am still alive, so they will own it wMany, many unintended problems could arise when you add co-owners to your property. The most obvious is your loss of ownership and control over the property, as the co-owner owns their share now, not after you die. You might become a party to a lawsuit of the co-owner, and you might lose the asset to a creditor of the co-owner. There may very likely be tax implications that must be carefully considered. If the property is real estate, there are many more legal issues that could arise if you add a co-owner. Further, only specific forms of co-ownership will result in a surviving co-owner automatically owning the entire property.

-

Can’t my spouse (or child) just go to the bank and close my account after I die?If the account has a joint owner or is a “transfer-on-death” account, then rules for those types of accounts will apply. However, if you are the sole owner of the account, then after your death, nobody has authority to access those funds unless the Surrogate’s Court gives them that authority.

-

What is the difference between a will and a living will?Do not confuse a will (a last will and testament) with a living will. A Last Will and Testament (or a “will”) is only operative after someone passes away. A Living Will is only operative during one’s lifetime. A Last Will and Testament, also referred to as a “will,” sets forth a person’s wishes regarding the disposition of their property upon their death. On the other hand, a Living Will is a document which sets forth your wishes regarding your end-of-life health care. A Living Will exists as a written proof of your desires regarding such issues as withholding life support, and can be used as evidence of your wishes when you cannot speak for yourself.

-

What is the difference between a will and a trust for asset distribution purposes?Both a will and a trust are effective estate planning documents that guide the disposition of one’s assets, but in different ways. Both a trust and a will are legal documents that express an individual’s wishes as to the distribution of his or her assets after lifetime. But whereas a will would only go into effect after the individual’s lifetime, and only through a court process known as “probate,” a trust is a legal entity of its own that can be established and take effect during an individual’s lifetime, and avoid the court process for any assets transferred to the trust during lifetime. It is common to prepare both a will and a trust in estate planning. Here are some main differences between a trust and a will:

-

Do I really need a will?Without a properly written will, you are giving up your legal right to decide who will receive your property after your death, and who will not receive your property. You may also be creating additional costs and complications for your heirs after you die. If you have minor children, you lose the opportunity to determine who will serve as guardian for them. The court will name the guardian and it may not be the family member or friend that you would want.

-

-

What Are The Essentials of a Solid Estate Plan?

-

At what age should I start thinking about estate planning?If you are 18 years or older, then probably now! It is never too early to think about your estate planning. Many people think that estate planning is a matter for the elderly, but that is not true. While people with greater assets often think about what will happen to them when they pass, it could be just as beneficial for the young to do the same. Even though people in their twenties may not own significant wealth, estate planning can help ensure your family has access to what assets you do own if something happens to you. The alternative can leave your family battling for access to your assets in court. Additionally, if you’re thinking that it may be beneficial to postpone estate planning because you know that your situation will change in the coming years, it is important to know that your estate planning documents can be changed as necessary. For example, if you are single and in your mid-twenties when you first start your estate planning documents, your documents can be changed upon the celebration of a marriage, the adoption or birth of a baby, and any other changes in circumstance.

-

Can changes be made to my estate planning documents?Almost all the time, the answer is yes. As long as you have capacity, your estate plan is an evolving process that should be revisited and modified as your health, wealth, and other personal circumstances change. It is always advisable to prepare the least restrictive plan possible to achieve your objectives so that modifications could be made as your personal situation changes. Although traditionally a will could be revised with a “codicil: to the will, which is a document that amends the will without revoking it, it is almost always preferable to have a new will prepared which revokes your existing will and supersedes the prior one. As for trusts, it will depend on whether the trust is revocable or irrevocable. Revocable trust, in nature, allows for modification and revocation of the document. On the other hand, with an irrevocable trust, the modifications are more difficult. The ability to modify an irrevocable trust will depend on the language provided in that specific trust. Since the flexibility for modifying an irrevocable trust is much more limited, it is advised that the trust documents be drafted in such a way to consider possible life changes.

-

How often, if ever, should I review my estate planning documents?Generally, you should revisit your estate plan every 3-5 years or on the onset of a significant life changing event like marriage, the birth or adoption of a child, divorce, death of a family member, or a move to another state. When reviewing your estate plan, it may very well be that there is no need to revise or change anything, or it may require simply updating beneficiaries of your assets. But it is important to have this review because even if you don’t feel that your situation changed, it is possible that laws may have changed that could affect your plan.

-

Why is estate planning important for my family’s future?Estate planning has many benefits. First, you can ensure your assets are distributed to the people you choose. Second, you can ensure that if you passed away your minor children would be cared for and their inheritance managed by the people you trust. Third, estate planning can minimize taxes or preserve your estate from being reduced due to the high cost of long-term care during your lifetime. That could mean more options for you during your lifetime and a greater inheritance for your loved ones. Fourth, you are making it easier for your children or other loved ones in the event of your incapacity and for after your lifetime. Fifth, you can protect the inheritance of any child or grandchild that has special needs. Sixth, you can make provisions for any children with specific issues such as alcohol abuse, creditors, or marital issues. So even if you do not wish to prepare your estate planning for yourself, you should consider estate planning as a gift for your children or loved ones.

-

An attorney prepared my parent’s Durable Power of Attorney and I presented it at my parent’s bank. The bank said that it has toTell the bank that New York General Obligations Law, Article 5, Section 1504-1 says that in the absence of reasonable cause, they must honor a properly executed power of attorney. In addition, recent amendments to the law now allow a court to award damages, including attorney’s fees and costs, if a proceeding is brought to compel acceptance of a power of attorney that was unreasonably rejected.

-

Can’t my spouse or children just take care of things if I cannot?If you become unable to act for yourself, nobody can just take over and sign your name for you. A bank or insurance company will not speak with anyone else but you without their proper legal authority. If you do not have a properly signed Durable Power of Attorney in place, a relative or friend would have to petition the court to make a declaration regarding your competence and appoint someone called a “guardian” to act for you. Guardianship proceedings can have a high cost, both in terms of time and money.

-

If I am joint owner on everything with my spouse, do I still need a power of attorney?Yes, it is still a critical document. While a Durable Power of Attorney may not be necessary for your spouse to access money in accounts held jointly with him or her, a Durable Power of Attorney goes beyond paying bills and dealing with bank accounts. In the event of incapacity, a Durable Power of Attorney would be critical in many scenarios. A durable power of attorney may be necessary to deal with insurance matters, arranging payment plans for doctors, applying for Medicaid for long term care needs (home health aide, or nursing home), establishing a trust for your benefit to preserve your money or joining a program to access or maximize government benefits, selling or buying a home, dealing with a mortgage or other loan, to name a few. Even if you own your home jointly with your spouse, if you lost mental capacity, your spouse wouldn't be able to manage real estate issues on your behalf, such as selling your home, without a durable power of attorney in place. Further, some institutions and residences wouldn’t accept a new resident if there wasn’t an effective power of attorney in place. Think about anything in the world that you sign for on your own behalf – if you were incapacitated, you would want the peace of mind knowing that the person you choose and trust can deal with whatever financial or legal situation arises to best address your needs.

-

What are the most important estate planning documents every adult should have?Typically, a comprehensive estate plan will consist of documents that address your estate both during lifetime and after lifetime. The documents that relate to after lifetime, address what you leave behind after your death, and may consist of a Last Will and Testament and/or trusts. However, documents that relate to during lifetime could be just as important, if not more important. These documents are known as “Advance Directives” and address important decisions and legal authority in the event you became incapacitated. Advance Directives include a Durable Power of Attorney (to appoint an agent for legal and financial matters), Health Care Proxy (to appoint an agent for health care decisions), and sometimes, a Living Will as well.

-

Are there any other documents?Our firm generally prepares a HIPAA Authorization which gives your health care agents the authority to receive your medical records. The HIPAA Authorization is very helpful because it provides the people you choose legal authority to obtain medical information and records on your behalf while you have capacity (and before the Health Care Proxy would take effect). We may also prepare a Designation of Burial Agent which would give the person you grant the authority to make burial decisions when you pass away.

-

Do I need a living will?A living will is a document which sets forth your wishes regarding your end-of-life health care. A living will exists as a written proof of your desires regarding such issues as withholding life support, and can be used as evidence of your wishes if you cannot speak for yourself. If there is any doubt that your health care proxy’s decision is not in accordance with your wishes, the living will would come into play. There are heavy considerations when deciding whether to sign a living will, so best to speak with your health care provider, and your attorney, prior to signing a living will.

-

Can’t my family speak to doctors if I am unconscious?Well, New York’s Family Health Care Decisions Act (FHCDA) allows certain family members or close friends to make health care decisions for patients if they are unable to speak for themselves. But New York Public Health Law gives competent adults a proactive powerful way to control their medical treatment even after they lose decision-making capacity, by allowing a competent adult to appoint someone they trust to make medical decisions on their behalf in the event they become unable to do so. The FHCDA is not intended to take the place of appointing a health care proxy. There are several disadvantages to relying on the FHCDA and choosing not to appoint a health care proxy. The law designates an order of priority for the person who can act as surrogate decision maker. The law may give authority to persons you would not want making health care decisions for you. Additionally, if you have several adult children, the law does not clarify which of your children have priority if they disagree. There are other limitations as well. It is best to have a Health Care Proxy that clearly designates the person that you wish to make crucial health care decisions for you, in the event you are unable to make decisions for yourself due to incapacity.

-

Why do I need a Durable Power of Attorney?A Durable Power of Attorney allows you to appoint a person you trust, called an “agent” to handle legal and financial matters on your behalf. It is called a Durable Power of Attorney because the document remains valid, even if you become incapacitated. A sudden injury or illness, or progressive dementia, are events that could result in a person’s incapacity. You may not need anyone to handle these matters on your behalf now, but if you do not prepare a Durable Power of Attorney while you are capable of doing so, then it will be too late if you should become incapacitated.

-

Can’t I simply download a Power of Attorney from a website? Isn’t it a statutory form?Yes, it is true that New York State law provides specific language to be used in a Durable Power of Attorney, but there are many reasons why a person would want to have an attorney prepare the form and oversee the signing of the form. First, the document can potentially give broad authority to your agent. You should be sure that you completely understand the document, and that you have any questions answered by an attorney, as the document advises on the first page. Second, the document is rather complicated, without an attorney advising you, you are at risk to incorrectly complete, initial, and sign the document. Third, there are powers that an agent may need in the future which are not listed and can not be granted by using the statutory form. Specifically, an Elder Law attorney would add many powers specific to your situation, or as may be required in the future. As an example, without additional provisions, your agent may not have the power to preserve assets in the context of Medicaid planning or proceed with tax planning to minimize estate taxes. The cost of not having a qualified Elder Law attorney prepare the power of attorney would seriously outweigh the cost of retaining an attorney to do so.

-

How do I know that my “agent” will do the right thing?The person that you appoint as your agent enters into a fiduciary relationship with you. Under the law, the fiduciary owes you a duty of trust and confidence. The agent must act according to any instructions you have provided or, where there are no specific instructions, in your best interest. But remember that even though the law states that your agent may be liable under the law for his violation, if it is found that your agent has acted outside the authority granted to him in the Power of Attorney and has not acted in your best interest, there is no “power of attorney” police looking over your agent’s actions. Therefore, you should always choose an agent who you totally trust.

-

Do I lose control if I have appointed an agent under a Durable Power of Attorney?No. You do not lose your authority to act, even though you have given your agent authority similar to yours. You may choose to keep your original documents yourself, but in a place accessible to your agent in an emergency. Your agent should be on standby and should not act if you could manage your own affairs, unless you have instructed him or her to assist you. Some people choose to give their agent the original power of attorney as soon as they sign it, with the belief that while they still have capacity, they can “test” their agent to ensure that the agent is trustworthy and acting in accordance with their wishes. Others, prefer not to give their agents the document, and only leave it in a place that is accessible to their agent in case of emergency. Something to think about: If you don’t trust your agent to act in your best interest while you have capacity to see what they are up to, they may not be the best person to act as agent when you lose capacity, when you can no longer oversee their actions.

-