Table of Contents

Long Island Trust Lawyer

A trust can be an important planning tool to manage your assets, as well as for passing your assets on to your loved ones. While trusts may offer exceptional benefits to those with substantial assets, a trust can be used in many different situations.

In fact, people may fail to appreciate the power a trust can have as a part of a well-crafted estate plan—a costly mistake. Trusts can be both flexible and powerful, containing instructions as to how and when to pass your assets on to your beneficiaries.

Not only can a trust help keep your affairs private and allow your loved ones to avoid the probate of your estate, but a carefully crafted trust can also have the added benefit of minimizing or even eliminating, estate taxes. A trust can preserve your assets in the event you need long term care and can also help you gain control over the distribution of your assets.

An effective trust is one that is carefully drafted by a qualified attorney who has a comprehensive knowledge of your specific situation, as well as a deep knowledge of current laws. After a thorough, thoughtful evaluation, an estate planning attorney from Esther Schwartz Zelmanovitz, PLLC can help determine if a trust is right for you, and, if so, which type of trust is most appropriate for you.

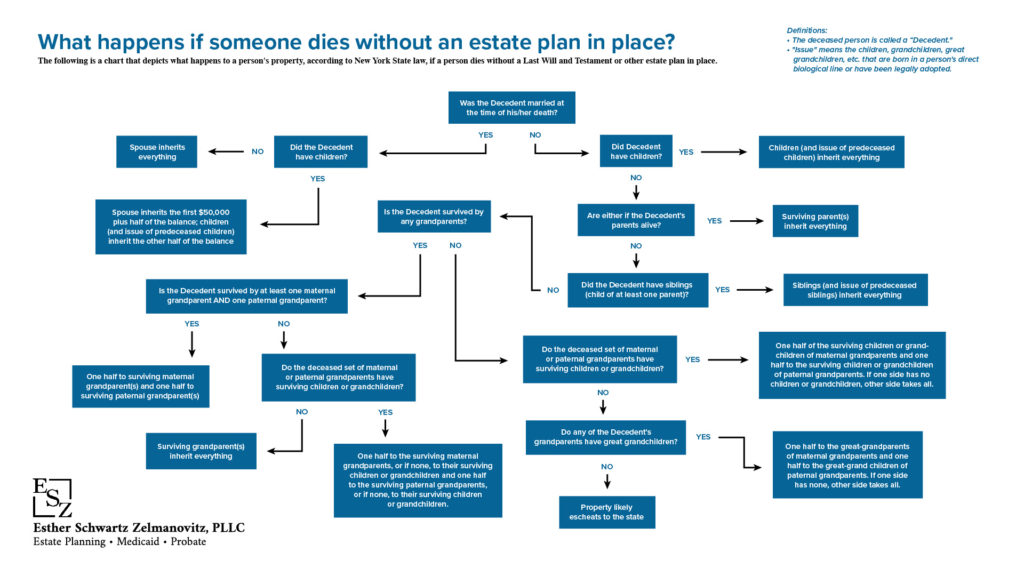

What happens if someone dies without an estate plan in place?

CLICK TO DOWNLOAD THE FULL CHART.

What is a Trust?

Essentially, a trust is a legal structure that contains instructions that dictate how and when your assets will be passed to your beneficiaries. Heirs may not be able to reap the benefits of a trust unless the trust is drafted by a highly qualified estate attorney.

A trust, unlike a will, is private. When a will goes through probate, it becomes open to the public, however, the contents of a trust remain private. Probate can also take a significant amount of time, sometimes more than a year. If you happen to own property in states other than New York, your heirs may be required to go through probate in each of those states.

A trust, on the other hand, seamlessly allows heirs to inherit without the delays and costs associated with probate. In short, you are able to have much more control over how your estate will one day be settled through establishing and funding a living trust. Some of the different types of trusts you might consider, according to your own circumstances, are detailed below.

Revocable Trust vs. Irrevocable Trust

Every trust is either a revocable trust or an irrevocable trust. As the names imply, a revocable trust can be changed or revoked entirely, while an irrevocable trust cannot.

While this is not an exhaustive list, both revocable and irrevocable trusts have the following benefits:

- Probate can be avoided, thus avoiding the cost, time, the public nature of probate, as well as the forum which allows creditor claims and contests.

- The estate and affairs remain private.

- There is much more flexibility and control over the distribution of assets.

- Provisions can be drafted to protect assets for disabled beneficiaries or beneficiaries that may have financial issues of their own.

- Continuity of asset management is maintained during disability of the grantor.

A revocable living trust can be amended at any time by the person who made the trust, which gives that person, known as the “Grantor” of the trust, much more flexibility. A Grantor can add property or other assets to the trust, or a Grantor can remove property if he or she wishes.

A revocable living trust is not, however a tax shelter. This means that income or dividends earned by the property held by the trust passes through the trust and is taxed to the Grantor directly. As noted, some of the advantages of a revocable living trust include avoiding probate court, avoiding guardianship proceedings to manage your funds, privacy issues, controlling the distributions of assets upon your death, and the fact that your assets become available almost immediately upon your death.

An irrevocable trust can provide the person who creates the trust additional benefits, however, the tradeoff is less flexibility, in that the irrevocable trust cannot be easily modified or revoked, if at all. Like a revocable trust, an irrevocable trust avoids probate, takes less time to administer and distribute the assets, and the details of the trust remain private.

When structured accordingly, assets in an irrevocable trust can be removed from your taxable estate, and the IRS will not count the trust assets for estate tax purposes. Assets placed in a properly drafted irrevocable trust can also be used to protect those assets from being considered for the purposes of qualifying for Medicaid. Finally, an irrevocable trust can also protect assets for a special need’s beneficiary, when correctly designed for that purpose.

Grantor Trust vs. Non-Grantor Trust

Every trust has either Grantor trust or a Non-grantor trust status. A grantor trust is a trust where the grantor retains certain rights over the trust and therefore, the income taxes earned on the trust assets is taxable to the grantor.

A Non-Grantor Trust is a trust where the grantor does not retain certain rights over the trust and therefore, income generated within the trust are not taxable to the grantor, but rather, the trust pays the income tax at the higher trust tax levels or each beneficiary will pay the tax on their proportion of distribution income received.

Revocable trusts are always grantor trusts, while irrevocable trusts can be designed as either a grantor or non-grantor trust, depending on the individual objectives and associated benefits.

Living Trust vs. Testamentary Trust

Every trust is either a living trust or a testamentary trust. A living trust is a trust is created during a grantor’s lifetime. A testamentary trust is a trust created under a person’s will, so is only created after death. There are advantages to setting up a living trust which can be managed and funded during your lifetime, without court intervention, and there are times when a testamentary trust is a more appropriate option. This would be determined based on each person’s specific objectives and needs.

Some specific types of trusts include:

- Medicaid Trusts are trusts which protect assets from being spent down on long-term care. A Medicaid trust is an irrevocable trust which protects one’s assets so that a person can qualify for Medicaid to pay for their long-term care (nursing home, home care, or in some instances, assisted living) without the need to spend down their money that is placed in the trust. In New York, Medicaid has a five-year look-back period for nursing home care eligibility, so to ensure that Medicaid will cover your long-term nursing home care costs without a penalty, it is ideal to fund a Medicaid Trust as early as possible, with the aim of at least five years passing before there is a need for a nursing home.

- Irrevocable Life Insurance Trusts are trusts which minimize estate taxes by removing a life insurance policy from being counted as part of the estate for tax purposes. An irrevocable life insurance trust is funded with a life insurance policy. You might wonder why you would choose an irrevocable life insurance trust as opposed to simply naming a beneficiary to your life insurance policy. The potential legal and financial benefits to heirs with an irrevocable life insurance trust include removing the life insurance proceeds from being counted as part of your estate for estate tax purposes, asset protection for beneficiaries, and your ability to direct and control the distribution of the proceeds with greater detail than by simply naming individual beneficiaries outright.

- Credit Shelter Trust/Disclaimer Trust/Marital Exemption Trust are trusts that are created under a person’s will or within their existing trust to minimize the effect of estate tax and remove assets from a surviving spouse’s estate. These trusts are irrevocable trusts, designed to drastically reduce or eliminate federal estate taxes for a married couple’s estate by taking advantage of each of their individual federal and estate tax exemptions. Depending on how it is structured, the trust may hold the assets of the first spouse to die. Rather than passing those assets along to the surviving spouse, the assets are removed from the surviving spouse’s taxable estate, diminishing estate tax liability. Your surviving spouse will retain certain access rights to assets, even though those assets are held in trust. Essentially, the assets bypass your surviving spouse’s estate after your death. When the surviving spouse dies, the assets are distributed to the trusts’ beneficiaries.

- Special Needs Trusts, also known as Supplemental Needs Trusts, are trusts that are designed to allow a disabled individual that is receiving government benefits, such as Medicaid or SSI (Social Security Income) to use and enjoy assets held in the trust without risk to interruption of discontinuance of their need-based government benefits.

There are a number of other trusts to suit each specific need. While the above are general types of trusts, there is no trust that is a “one-size-fits-all.” Every trust has specific provisions tailored for each individual’s unique needs.

Can I Amend My Living Trust Without an Attorney?

As with preparation of an original living trust, an amendment to a living trust may have serious legal ramifications. It can seem very simple to change one sentence, or one provision in your trust, and believe that your updated wishes have been adequately reflected in your trust and will be enforced, but there are many legal issues to consider when even the most simple change is made to your trust. By explaining your objective to an experienced estate planning attorney that knows the law relating to trust drafting and trust administration, he or she will be able to identify any issues that can arise with your desired revision to your trust and ensure that the intended change will have the intended result and that your plan remains effective.

It is too often that attorneys assist with trust administration, after the death of the trust grantor, and find invalid revisions, or amendments that have unintended consequences because the amendments were not done under the guidance and supervision of an experienced trusts attorney.

Do I Need a Lawyer to Prepare My Trust?

A trust is essentially an agreement between a “grantor” and a “trustee” to manage assets that would benefit a “beneficiary” or group of beneficiaries. You may think you can simply make a trust arrangement on your own by downloading a form from the internet. That being said, a trust can have serious consequences if not done correctly, whether critical provisions are missing, or incorrect provisions are added to a trust, wrong choices are made with regard to appointing a trustee or naming beneficiaries, or most commonly, when a trust is not funded correctly, or sometimes not even funded at all!

Without the proper guidance and broad review of the circumstances surrounding the trust, a trust can easily miss your estate planning or other objectives, and the “trust” wouldn’t be worth the paper it’s written on.

So to answer the question, yes, it is strongly recommended to not only retain a lawyer to prepare your trust, but to retain an estate planning lawyer that is specifically experienced with trusts.

Getting the Help You Need in Establishing a Trust from Esther Schwartz Zelmanovitz, PLLC

At Esther Schwartz Zelmanovitz, PLLC, we are dedicated to providing you with honest, knowledgeable counsel and can carefully guide you in choosing the best type of trust for your situation. We understand the importance of estate planning, as well as the long-lasting effects it can have on both you and your loved ones. We will provide highly customized solutions uniquely tailored to fit your needs.

If you are considering establishing a trust, contact our legal team to discuss the various legal options available to you. It is important that you be proactive when planning your estate. Our top-rated law firm, located in Great Neck, NY, will facilitate your legal needs by making home visits and evening appointments available. We serve your legal needs in Long Island, all five boroughs of New York City, and across the state.