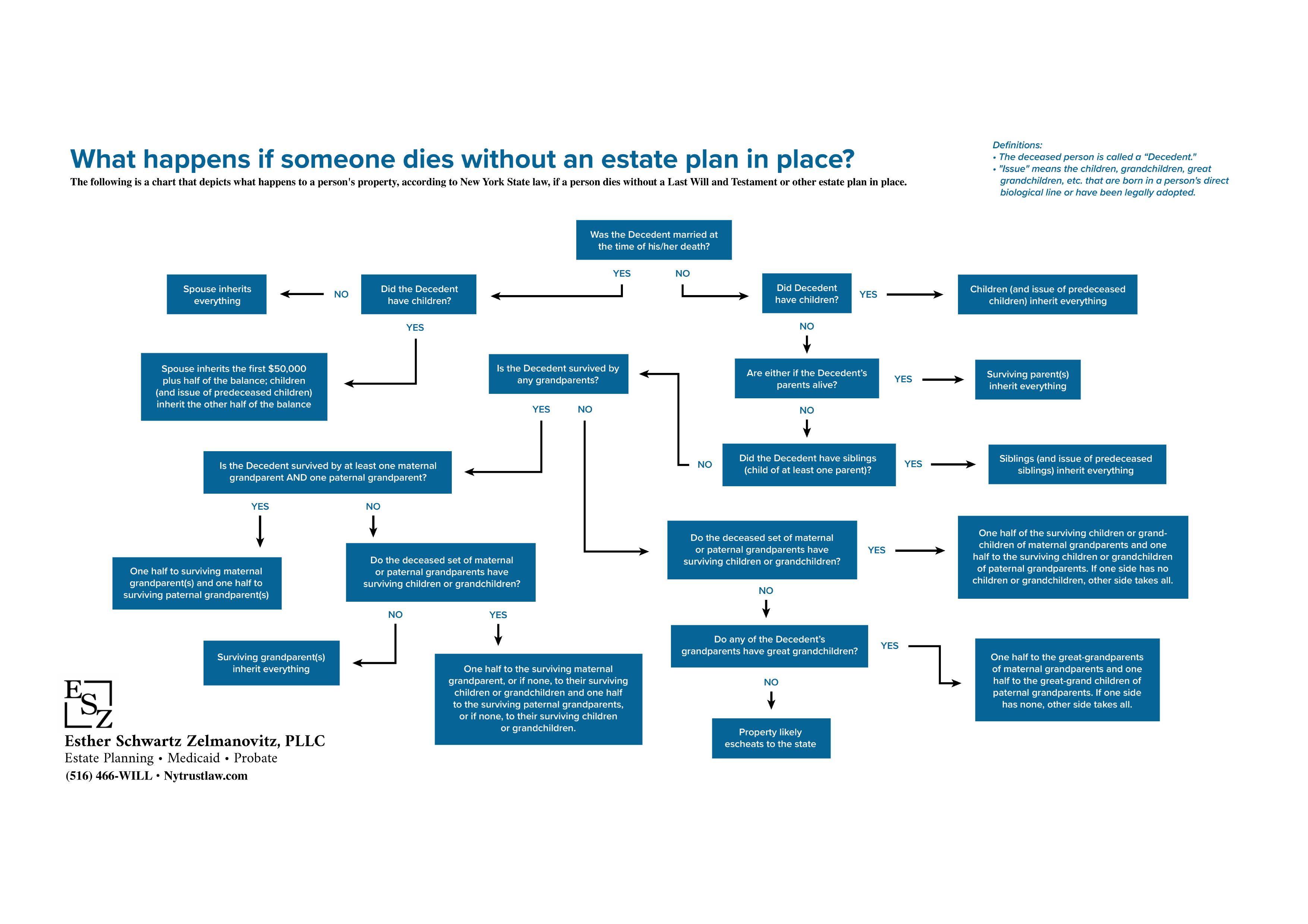

Medicaid Planning & Applications for Home and Nursing Home Care

Medicaid is the government-funded, nationwide, state-specific program through which many persons receive care at home or in a nursing home. The program is currently administered through the Department of Social Services–with the exception of the five counties which comprise metropolitan New York, which are administered through the Human Resources Administration.

The Medicaid application process can be both complex and confusing, with eligibility rules and application processes differing from program to program. It is important that you be wary of offers to prepare your Medicaid application free, or at a significantly reduced rate—remember the old adage that if it sounds too good to be true, it probably is.

What is required is a comprehensive knowledge of New York Medicaid rules, experience helping others obtain Medicaid benefits, and the necessary skillset to make it happen. Because the law has so many intricacies and nuances, having an experienced Esther Schwartz Zelmanovitz, PLLC attorney by your side will ensure you are fully informed of all the legal issues related to Medicaid, and that all your questions are properly answered. Your elder law attorney does not work for the nursing home and has an ethical duty to advocate on your behalf, and only for your interests.

Why is Medicaid Necessary for Home Care and Nursing Home Situations?

Long term care in New York, including home health care, assisted living facilities, and nursing homes, is very expensive. In fact, in 2023, the average cost of a nursing home on Long Island, New York, was a staggering $169,632 per year ($169,704 in New York City). Medicare generally does not cover nursing homes, and neither does private health insurance. This leaves Medicaid for many New Yorkers who require long term care.

A person does not necessarily have to first spend all their assets before qualifying for Medicaid. The attorneys at Esther Schwartz Zelmanovitz, PLLC, can help preserve your assets while also qualifying for Medicaid. Medicare pays for very limited costs associated with long term care, and Medicaid can step in when a person’s resources are exhausted, or with the help of an Elder Law attorney, when his or her funds have been legally and properly transferred.

Medicaid Long Term Care

When you need a home health aide, or must enter a nursing home or assisted living facility, you can either pay the costs out-of-pocket by using your income, assets, and savings, or you can apply for Medicaid to pay for your home health aide, nursing home, or, in some instances, assisted living facilities that accept Medicaid.

While paying for your own home health aide, nursing home or assisted living facility obviously requires the least amount of advance planning, the cost is high and can end up taking every single dime you have amassed throughout your lifetime, leaving nothing for those who would otherwise inherit. Because of this, it is worthwhile to explore alternative methods of covering the costs associated with long term care.

The passage of the Deficit Reduction Act of 2005 created a five-year “lookback” period for the transfer of assets. This means that if transfers are made within the lookback period, which fails to meet certain rules, a penalty period will be triggered. During the penalty period, the recipient is ineligible to receive Medicaid benefits.

Our Values, Your Peace of Mind The Principles That Define Our Firm

-

Compassionate, Relationship-Driven Service

We believe every client deserves to be treated with dignity, patience, and genuine care. Our firm fosters long-term relationships, guiding families with warmth and empathy through emotionally sensitive matters like elder care, estate planning, and loss.

-

Clear, Respectful Communication

We prioritize honest, prompt, and respectful communication. Whether answering questions or guiding you through complex decisions, we're responsive, dependable, and committed to making the process as smooth and stress-free as possible.

-

Serving with Integrity and Excellence

We hold ourselves to the highest standards of ethical practice and professional excellence. Clients can count on us not just for our legal knowledge, skill and experience, but for honesty, transparency, and unwavering advocacy on their behalf.

-

Tailored Legal Guidance for Every Client

No two clients are the same. We take the time to truly understand each client’s concerns, goals, and values, crafting customized legal solutions that reflect what matters most to them.

Planning Strategies Which Can Provide Medicaid Eligibility Along with Peace of Mind

Recommended reading: NYS Income and Resource Limits for Medicaid (2026)

There are a number of strategies that can help those who want to qualify for Medicaid while retaining their savings. In the state of New York, the total resource allowance (as of 2023) for an individual receiving Medicaid home care (or “community based”) services is $28,133 or $37,902 for a couple.

The attorneys at Esther Schwartz Zelmanovitz, PLLC can determine the best planning strategy for maximum preservation of your assets, based on your particular situation and personal long term needs. Some planning strategies may include setting up an irrevocable trust, First-Party Special Needs Trust, Third-Party Supplemental Needs Trust, spousal transfers, transfers to a disabled child, promissory note/gift planning, and various other transfers and spend-down strategies.

In the state of New York, the total income allowance (as of 2023) for an individual receiving Medicaid home care (or “community based”) services is $1,563 or $2,106 for a couple. If a New York State resident is receiving Medicaid Home Care services, he or she would be required to pay any income over the Medicaid limit to the Department of Social Services (or Human Resources Administration, if a New York City resident).

In the alternative, an individual would be able to maintain their Medicaid eligibility by joining a pooled income trust as a method of setting aside any excess income for the Medicaid recipient’s use, while still qualifying for Medicaid. New York State allows recipients of nursing home services to keep only $50 a month for themselves. A nursing home resident’s spouse, known as the “community spouse,” has a monthly maintenance needs allowance of $3,715.50. This means that if their own income is less than that amount, they can keep a portion of their nursing home spouse’s income to meet that limit.