Medicaid is the government-funded, nationwide, state-specific program through which many persons receive care at home or in a nursing home. The program is currently administered through the Department of Social Services–with the exception of the five counties which comprise metropolitan New York, which are administered through the Human Resources Administration.

The Medicaid application process can be both complex and confusing, with eligibility rules and application processes differing from program to program. It is important that you be wary of offers to prepare your Medicaid application free, or at a significantly reduced rate—remember the old adage that if it sounds too good to be true, it probably is.

What is required is a comprehensive knowledge of New York Medicaid rules, experience helping others obtain Medicaid benefits, and the necessary skillset to make it happen. Because the law has so many intricacies and nuances, having an experienced Esther Schwartz Zelmanovitz, PLLC attorney by your side will ensure you are fully informed of all the legal issues related to Medicaid, and that all your questions are properly answered. Your elder law attorney does not work for the nursing home and has an ethical duty to advocate on your behalf, and only for your interests.

Table of Contents

Why is Medicaid Necessary for Home Care and Nursing Home Situations?

Long term care in New York, including home health care, assisted living facilities, and nursing homes, is very expensive. In fact, in 2023, the average cost of a nursing home on Long Island, New York, was a staggering $169,632 per year ($169,704 in New York City). Medicare generally does not cover nursing homes, and neither does private health insurance. This leaves Medicaid for many New Yorkers who require long term care.

A person does not necessarily have to first spend all their assets before qualifying for Medicaid. The attorneys at Esther Schwartz Zelmanovitz, PLLC, can help preserve your assets while also qualifying for Medicaid. Medicare pays for very limited costs associated with long term care, and Medicaid can step in when a person’s resources are exhausted, or with the help of an Elder Law attorney, when his or her funds have been legally and properly transferred.

As of 2011, Medicaid paid for the care of almost 70 percent of nursing home residents. Medicaid recipients must contribute virtually all of their income toward the cost of long term care, usually retaining only a small monthly allowance for personal needs.

Additionally, states are allowed to recapture the costs of nursing home care by placing a lien on the resident’s property and by collecting from the estate of the resident after his or her death. This is the primary reason for early planning—your New York estate planning attorney can help you create an estate plan which protects your assets yet allows you to be eligible for Medicaid benefits.

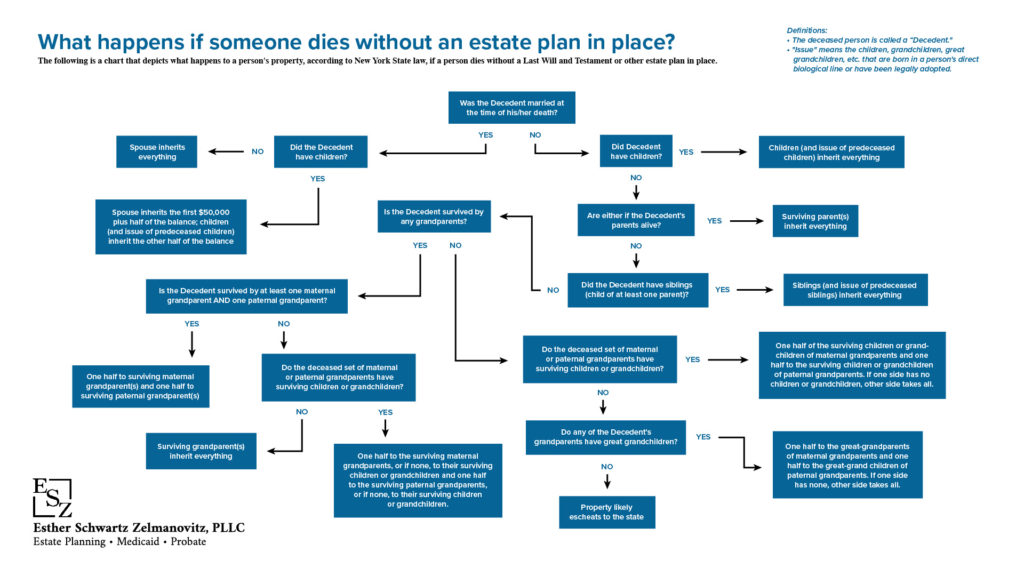

What happens if someone dies without an estate plan in place?

CLICK TO DOWNLOAD THE FULL CHART.

Medicaid Long Term Care

When you need a home health aide, or must enter a nursing home or assisted living facility, you can either pay the costs out-of-pocket by using your income, assets, and savings, or you can apply for Medicaid to pay for your home health aide, nursing home, or, in some instances, assisted living facilities that accept Medicaid.

While paying for your own home health aide, nursing home or assisted living facility obviously requires the least amount of advance planning, the cost is high and can end up taking every single dime you have amassed throughout your lifetime, leaving nothing for those who would otherwise inherit. Because of this, it is worthwhile to explore alternative methods of covering the costs associated with long term care.

The passage of the Deficit Reduction Act of 2005 created a five-year “lookback” period for the transfer of assets. This means that if transfers are made within the lookback period, which fails to meet certain rules, a penalty period will be triggered. During the penalty period, the recipient is ineligible to receive Medicaid benefits.

This penalty period has the ability to bring devastating consequences to one’s financial savings and to the care they receive. In New York, the lookback period is five years for nursing home care and while recent law imposed a thirty (30) month lookback on community care, the earliest it is expected to be implemented in April 1, 2024. Because the rules are both specific and complex, it is highly advisable that you do your planning in advance—doing so brings the greatest likelihood that five years will pass prior to the time long term care is necessary.

In some instances, even when a long term care plan has not been set up five years prior to entering a nursing home, there is an opportunity for “crisis planning.” Should you find yourself in this position, Esther Schwartz Zelmanovitz, PLLC can assist you in preserving the maximum level of your savings and assets without sacrificing the level of care. This could come in the form of exempt transfers, spend-downs, and gift/promissory notes.

In addition to determining the financial eligibility of a person in need of long term care services, Medicaid evaluates eligibility based on a physical assessment as well. Medicaid pays for nursing home care when skilled care is required. Medicaid pays for home care only when the individual requires assistance with activities of daily living (ADL); the number of hours and days provided will be based on the ADL assessment.

Planning Strategies Which Can Provide Medicaid Eligibility Along with Peace of Mind

Recommended reading: NYS Income and Resource Limits for Medicaid (2023)

There are a number of strategies that can help those who want to qualify for Medicaid while retaining their savings. In the state of New York, the total resource allowance (as of 2023) for an individual receiving Medicaid home care (or “community based”) services is $28,133 or $37,902 for a couple.

The attorneys at Esther Schwartz Zelmanovitz, PLLC can determine the best planning strategy for maximum preservation of your assets, based on your particular situation and personal long term needs. Some planning strategies may include setting up an irrevocable trust, First-Party Special Needs Trust, Third-Party Supplemental Needs Trust, spousal transfers, transfers to a disabled child, promissory note/gift planning, and various other transfers and spend-down strategies.

In the state of New York, the total income allowance (as of 2023) for an individual receiving Medicaid home care (or “community based”) services is $1,563 or $2,106 for a couple. If a New York State resident is receiving Medicaid Home Care services, he or she would be required to pay any income over the Medicaid limit to the Department of Social Services (or Human Resources Administration, if a New York City resident).

In the alternative, an individual would be able to maintain their Medicaid eligibility by joining a pooled income trust as a method of setting aside any excess income for the Medicaid recipient’s use, while still qualifying for Medicaid. New York State allows recipients of nursing home services to keep only $50 a month for themselves. A nursing home resident’s spouse, known as the “community spouse,” has a monthly maintenance needs allowance of $3,715.50. This means that if their own income is less than that amount, they can keep a portion of their nursing home spouse’s income to meet that limit.

How We Can Help You with Your Medicaid Planning and Medicaid Application for Long Term Care

At Esther Schwartz Zelmanovitz, PLLC, we give individualized attention to each and every client, carefully crafting a solution that is tailored to your unique situation. You can expect your Medicaid application to be completed in a professional manner by our experienced attorneys. We are committed to helping you find peace of mind through high-quality representation, proven strategies, and exceptional service. The earlier you plan for your long term care, the more options you will have, along with the highest level of flexibility.

The attorneys at Esther Schwartz Zelmanovitz, PLLC will help you preserve your long term assets. When an experienced elder law attorney prepares your Medicaid application, and is there to provide you with planning advice associated with your long term care needs, the long term financial effects on you and your loved ones are significantly minimized and preservation of assets maximized. Esther Schwartz Zelmanovitz, PLLC, serves your legal needs in Long Island, all five boroughs of New York City, and across the state. Home visits and evening appointments are available for your convenience, so contact Esther Schwartz Zelmanovitz, PLLC, today.